Bauxite developer CAY to acquire 9.1% of Cameroon rail company, plus board seat

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 2,307,692 CAY shares at the time of publishing this article. The Company has been engaged by CAY to share our commentary on the progress of our Investment in CAY over time.

Canyon Resources (ASX:CAY) owns one of the world’s richest bauxite deposits.

CAY’s project has a 1 billion tonne JORC resource with an ore reserve of 109Mt, in Cameroon.

Bauxite is the primary input needed to produce aluminum - a critical metal for industries like defense, construction and electrification.

The bauxite price has been rising and rising over the last few years...

Because of fears the world’s biggest exporter would impose export restrictions and create supply shortages - read our full analysis here (14 min read).

A 2022 feasibility study showed CAY’s project would have a Net Present Value (NPV) of US$452M using a US$45/tonne bauxite price.

The bauxite price has more than doubled to over US$90/tonne since this study.

Plugging in today's bauxite prices more than quadruples CAY’s NPV number to somewhere between US$1.6 and US$1.9BN.

(more on those numbers later)...

Edison Investment Research released a report 2 weeks ago suggesting the project could make US$200M EBITDA a year when “fully ramped up" (read it here).

Note - this is based on a number of assumptions plugged into a spreadsheet - don’t rely on research report valuations alone when investing in speculative stocks.

CAY is 41.7% owned by a deep pocketed, major shareholder with experience in African resource projects. In January they underwote up to ~$124M in debt funding to CAY...

CAY’s project is also very high grade compared to other major bauxite deposits...

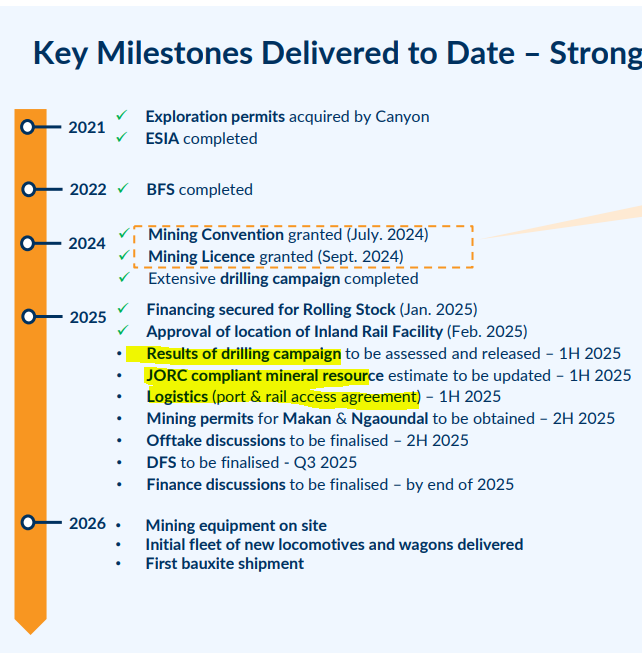

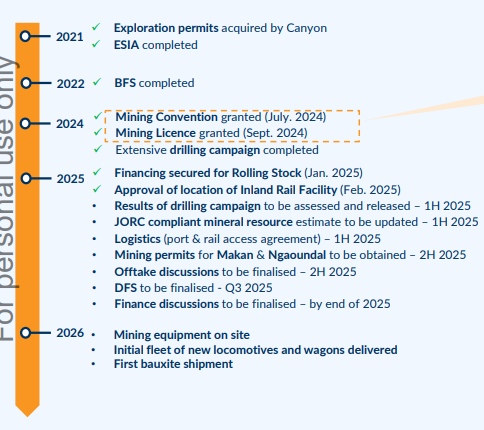

It's got a mining license and mining convention tucked away...

CAY says its “first bauxite shipment” is now coming in 2026....

BUT...

Bauxite is a bulk commodity. It’s heavy and hard to move around.

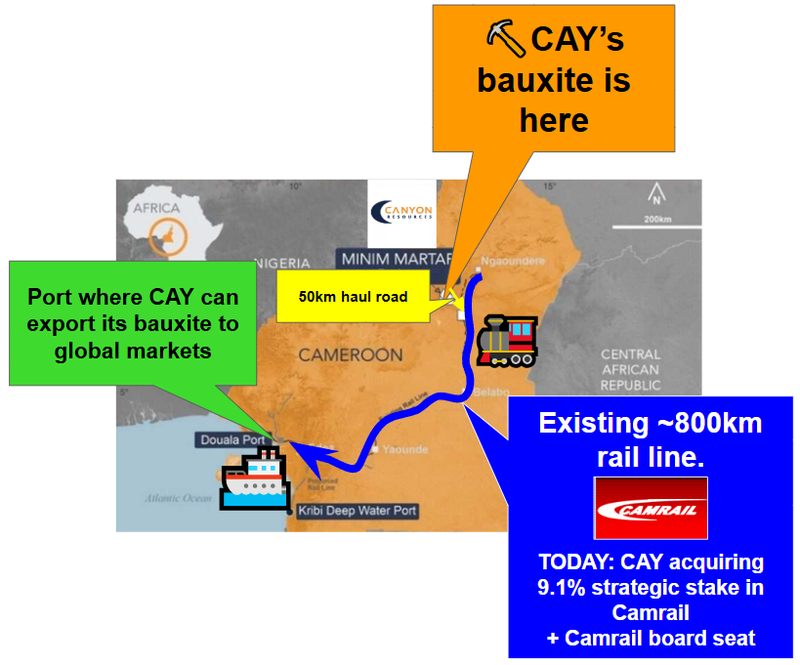

None of the above matters UNLESS a company can get tonnes and tonnes of the commodity onto a RAILWAY and to a PORT for export into global markets.

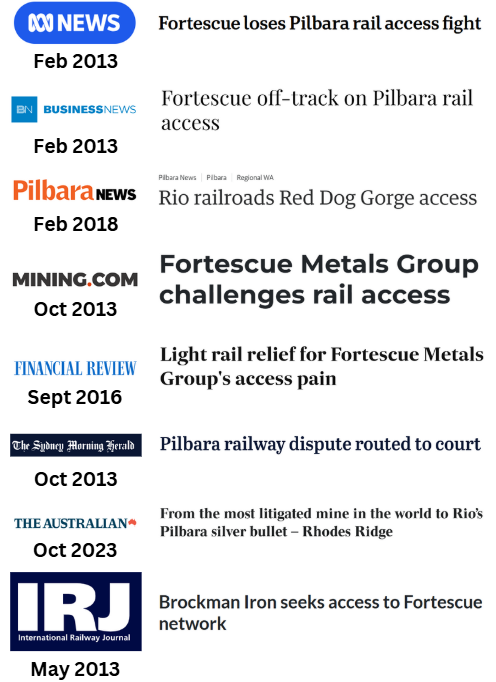

Many who followed the BHP, RIO and FMG “rail wars” in the 2010s know how important rail access to a port is for exporting bulk commodities (like iron ore or bauxite).

In order to have more control over its destiny, today CAY announced it is acquiring a 9.1% strategic stake in Camrail.

Camrail owns and operates the 800km railway linking CAY’s giant bauxite deposit to the port.

(Source)

The total consideration of approximately A$3.4M for the 9.1% holding will be paid from the company’s existing cash reserves (CAY had A$15.5M at the end of 2024).

Upon deal completion, CAY will nominate one board member to Camrail - giving CAY oversight and direct influence over this critical piece of project infrastructure.

Today’s news comes off the back of January’s announcement that CAY’s major shareholder agreed to underwriting US$124M for CAY to purchase the 22 locomotives and 550 wagons CAY needs to move their bauxite to port - read our analysis here (11 min read)

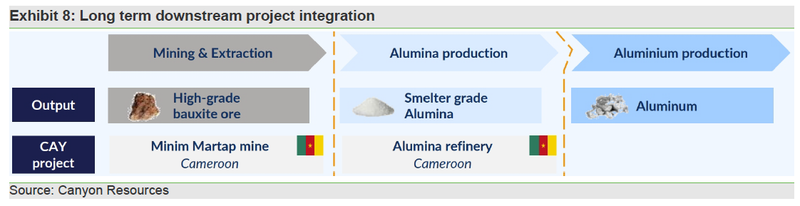

Speaking of CAY’s major shareholder, Eagle Eye - we noted some media speculation 4 weeks ago that they are in talks to buy a stake in or acquire Cameroon’s state aluminium company which owns the Edea Aluminium smelter - (read our analysis here (14 min read)

(Aluminium smelters process bauxite into aluminium - it takes 4 to 5 tonnes of bauxite to make 1 tonne of aluminium)

It appears there is a grand plan in place here...

Here is what we are expecting to see next from CAY over the next ~12 weeks that we think is important enough to move the share price:

- Drill results - CAY just finished drilling 1,526 boreholes for a total of 23,254m in drilling. The results should be out fairly soon (expected H1-2025) and will go toward the update to CAY’s JORC resource.

- Updated JORC Mineral Resource Estimate - ultimately, all the drilling CAY has been doing is to update (and hopefully upgrade) its 1 billion tonne JORC resource.

Beyond that, we are looking out for:

- Signed agreements for logistics partners - we want to see rail and port access agreements signed and finalised.

- Offtake’s & financing - CAY has said before that samples had been shipped to potential offtake partners, we want to see CAY lock in signed offtake agreements this year.

- Project financing - CAY’s already got ~50% of the project’s CAPEX underwritten by Eagle Eye (biggest shareholder). We want to see the rest of the project financing secured.

- Updated Definitive Feasibility Study (DFS) - Hopefully we see a big upgrade from CAY’s previous study done in 2022.

Why we liked today’s announcement

Bauxite is a Direct Shipping Ore bulk commodity - meaning mining and processing the rocks is relatively easy - the challenge is getting it from the mine site to the customers.

Rail and port access are dealbreakers for bulk commodity projects - so today’s news of CAY buying into Camrail is big news for CAY.

A good way of comparing just how important logistical infrastructure is for bulk commodities projects is to look at the WA iron ore industry.

Anyone who followed the rail access battles in the Pilbara between FMG, Rio and BHP will know how hard the companies fought over rail infrastructure.

Solving the “rail problem” is what made Fortescue the $49BN iron ore behemoth it is today - at the time a lot of the market thought they could never get it done...

Rail infrastructure is also a big part of the competitive edge that has made the Pilbara iron ore mines some of the lowest cost operations in the world.

After today’s news, CAY is buying its own slice of rail infrastructure - only this time the rail is already built.

It also means that CAY benefits from all the upgrades the rail infrastructure has seen over the last ~four years.

In 2021, around 68 rail bridges were upgraded, and the World Bank oversaw the refurbishment of ~330km of the 500km rail line that runs to CAY’s project.

Then in 2022 the EU agreed to fund ~€123M (of a total €243M funding) to upgrade another 330km of the rail line.

(Source)

So CAY is getting a lot for what we think is a relatively small capital outlay.

As mentioned earlier, CAY also gets a board seat on Camrail, which means its opinion will matter when things like rail upgrades are being discussed.

That board seat will come in handy when CAY is discussing how its US$124M rail fleet will integrate into the rail systems in country.

As we mentioned above, CAY’s biggest shareholder is underwriting ~US$124M in debt which would be used to cover the rail fleet CAY needs for its project.

(that amount is almost 50% of the project's total CAPEX...)

We covered that news in a detailed note a few weeks back: US$124M in financing now underwritten - CAY can buy trains to get its bauxite to market - 50% of CAPEX

So it's all happening for CAY AND it's happening where it really matters for a bulk commodities project - on the logistics front.

All of which is leading to the big catalyst - “first bauxite shipment” in 2026.

CAY is getting its project into production and re-rating from developer to producer is a big part of our Big Bet which is as follows:

Our Big Bet for CAY

“CAY takes its bauxite project into production is re-rated to a market cap greater than $1BN”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our CAY Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

New CAY presentation out this week - what has changed?

Earlier this week CAY presented at the PDAC conference in Canada.

PDAC is one of the biggest mining conferences in the world so it's good to see CAY up and about at one of these events.

At the conference, CAY presented its new deck which you can check out in detail here.

A key takeaway for us from the new preso was that CAY now seems to be a lot more specific with its references for when to expect key catalysts.

The last presentation from earlier in the year was a lot more vague with all of the catalysts falling into “2025”.

Now the company has specific quarter/half references for each individual catalyst.

Here were a few that stood out to us:

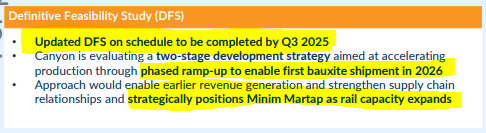

- CAY expects to have its updated Definitive Feasibility Study (DFS) completed by Q3 2025 .

- CAY also seems to be bringing forward its first production date to 2026. This is through a two phased development of the project - get the project into production then scale it up as infrastructure capacity increases in the country.

- CAY explicitly mentioned that signed agreements for rail and port access were expected to be completed inside the first half of 2025. So we can expect these within the next 3 months.

- We also saw that CAY is a lot more advanced with offtake negotiations than we initially thought.

CAY mentioned that product samples had already been sent to different groups and that offtake agreements were expected in H2 2025.

The following slide gave a pretty good overview of what to expect from CAY in the short/medium term.

It looks like almost every major catalyst is expected between now and the end of 2025 - leading up to first production in 2026.

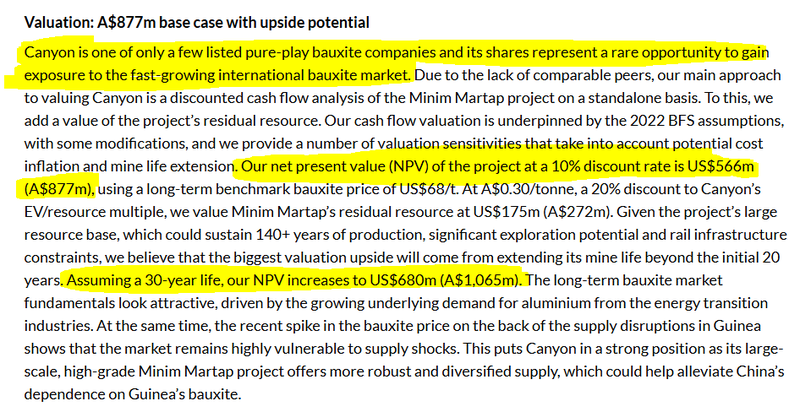

CAY research report values its project at up to A$1.07BN

Two weeks ago we came across a research report for CAY from London based Edison Investment Research, written by analysts Andrew Keen and Andrey Litvin.

Small cap stocks rarely ever get research reports written about them so it’s good to see someone lay out the CAY story in this format.

The report put a valuation on CAY’s project of A$877M with an upside case of A$1.07BN

While that valuation target does look interesting, we should be clear that analyst price targets are based on a number of assumptions that may be incorrect - they (or us) don't have a crystal ball. It’s definitely possible CAY does not reach this valuation. CAY is a high risk small cap stock. Never invest on a valuation target alone, and always do your own research.

Check out the full report here: Canyon Resources — Rapidly emerging bauxite producer

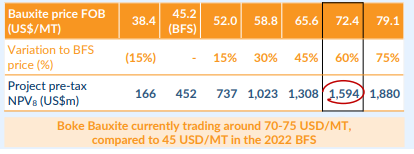

The Edison financial modeling was done using a US$68 per tonne bauxite price, despite recent prices hitting US$120 per tonne.

We did notice, in CAY’s recent investor presentation that by plugging in a US$72-79 per tonne price the project’s pre-tax NPV would jump to US$1.6BN to US$1.9BN.

That is currently more than 4x CAY’s current undiluted market cap of ~$355M.

(Source)

A substantial improvement if bauxite is in the US $70s - its currently in the US $90s.

A few things stood out to us from the report:

1. On CAY’s project and its financials:

- The report reiterates how there are very few exposures to bauxite on the ASX and especially at the size/scale of CAY’s project (in the small cap end of the market). This was one of the key reasons we made CAY our Wise Owl Pick of The Year for 2025.

- The report mentions explicitly how CAY’s project is unique from a capital efficiency perspective - Edison made reference to the US$426M investment by Chinalco into a 6mtpa bauxite project with a capital intensity of US$70 per tonne. This compares that to CAY’s project which has capital intensity closer to US$65 per tonne. A US$5 per tonne difference may not sound like much, but for a bulk commodities project where size/scale is everything, it's a big deal.

- CAY’s project, once developed up to a 6.4 Mtpa capacity would still have a 20 year+ mine life based on its current reserves. That 20+ year mine life is based on <10% of the project’s overall 1BN tonne JORC resource. So there is plenty of scope for this to be a multi decade producing asset...

- Edison estimated an NPV for the project using a bauxite price of US$68 per tonne of A$877M. (Keep in mind spot prices were almost double that recently at ~US$120 per tonne)

- At full capacity Edison’s modelling is estimating annual revenues of US$371M and EBITDA of US$200M. (applying a 10x multiple on that EBITDA, CAY could potentially trade at >A$2BN once fully ramped up with production).

2. On the quality of CAY’s resource:

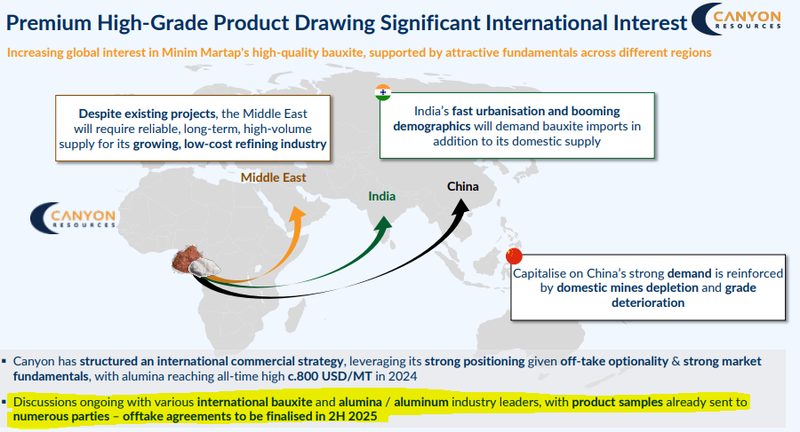

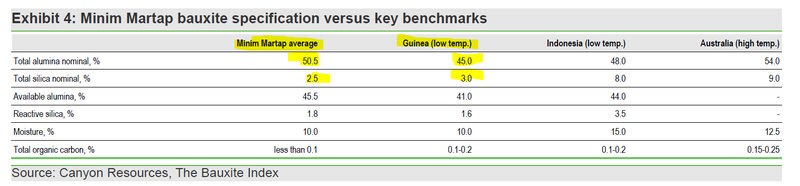

The report also talked about how CAY’s project stacks up against other bauxite from other jurisdictions (highlighting the low silica, high alumina %), which is good for showing how easily CAY’s bauxite can be processed into aluminium.

The main takeaway here is how well CAY’s resource stacks up against bauxite coming out of Guinea... (grades are a lot higher, and silica content lower)

3. On CAY’s strategic partnership with Eagle Eye Asset Management:

The report highlights how EEA has committed to up to US$123M in debt financing for the projects CAPEX (rail stock) which de-risks the project significantly from a financial perspective - covering ~50% of the projects required CAPEX.

Edison also made mention of the recent media reports that EEA were in talks with the Cameroon government over a state owned aluminium producer Alucam.

The report highlighted the potential for CAY’s project to be vertically integrated if EEA takes a stake in that company.

Today’s move, taking ownership in the rail company is further proof of this in play.

4. On logistical infrastructure:

This part of the Edison report is really helpful, especially after today’s news.

Edison highlighted all of the infrastructure upgrades that have gone on inside the country since 2021 (and explicitly mentioned the rail upgrades):

- Since 2021 ~68 rail bridges have been upgraded.

- ~330km of the 500km rail line that runs to CAY’s project has been refurbished.

- The state owned rail operator confirmed the rail lines are rated for 20-tonne loads and can accommodate the tonnages required by CAY.

- €243m of funding which is being used to upgrade another 330km of railway lines which expects to increase rail capacity even further by 2030.

- The port of Douala where CAY plans to ship its bauxite out of, recently received €142m in funding from the African Export-Import bank and €60m from a project company to upgrade its facilities.

- There is also a push to develop an industrial zone around the port which is expected to be completed by the time CAY is ready for ramp-up.

So Cameroon has a lot of capital going into port infrastructure and its road/rail network over the next five years.

From a CAY perspective that means that the project could be ramped up well beyond the 3.5mtpa production run rate that the 2022 Bankable Feasibility Study was based on.

With a 1BN+ tonne JORC resource and the infrastructure upgrades being completed, by 2030 it looks like CAY will have optionality around increasing that throughput as it sees fit.

This type of inherent upside in a project is what major players look for when considering potential takeovers. Assets they can operate efficiently and upscale/downsize as market demand changes

What we want to see next from CAY?

The slide below from CAY’s recent investor presentation gives a pretty good overview of what we can expect to see next:

(Source)

In the short term we are looking forward to seeing the results from the drill program, the upgrade to the JORC resource and of course, the results from the updated Definitive Feasibility Study.

That study was done using a US$45.20 per tonne bauxite price.

Bauxite prices are now above US$90...

We are expecting a big improvement in the Net Present Value (NPV) number when the updated DFS comes out in Q3.

As mentioned earlier, a slide from the recent presentation also gives us an idea of what we can expect to see...

Plugging in prices closer to today’s spot prices more than quadruples the NPV we saw in the 2022 feasibility study.

For some context, the old study had an NPV of US$452M from US$253M CAPEX over a 20-year mine life.

The slide below is showing US$1.6-US$1.9BN using US$72-79 per tonne bauxite prices.

(Source)

What are the risks?

While bauxite prices remain very strong, we are keeping our eyes peeled for any changes to the bauxite price - if the bauxite price falls this could hurt CAY’s share price.

Commodity price risk

CAY’s project is at the BFS stage, meaning it is highly sensitive to changes in underlying commodity prices. If the bauxite price were to fall it would hurt overall project economics and make it harder for CAY to lock in project financing for the development of the project.

Source: What could go wrong? - 20 January 2025 CAY Investment Memo

We are also paying attention to West African politics, in particular Guinea. Guinea may be considering a bauxite export ban, which it also may reverse away from. As Guinea is a major exporter of bauxite any change to the status quo here could alter the desirability of CAY’s project in the eyes of potential financiers.

Geopolitical risk

While we believe Cameroon’s current political climate is stable, there have been four coups in the last 4 years in the West Africa region. CAY’s project is subject to the volatility of doing business in this part of the world. Geopolitical risks form a significant part of CAY’s overall risk profile.

Source: What could go wrong? - 20 January 2025 CAY Investment Memo

We list more risks to our CAY Investment Thesis in our Investment Memo here.

Our CAY Investment Memo

You can read our CAY Investment Memo in the link below. We use this memo to track the progress of all our Investments over time.

Our CAY Investment Memo covers:

- What does CAY do?

- The macro theme for CAY

- Our CAY Big Bet

- What we want to see CAY achieve

- Why we are Invested in CAY

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.